Weekend Reading #367

This is the three-hundredth-and-sixty-seventh weekly edition of our newsletter, Weekend Reading, sent out on Saturday 6th June 2026.

To receive a copy each week directly into your inbox, sign up here.

*****

What we're thinking.

We are at the stage of the market move now where we honestly don't know how long we have left to go. It seems like nosebleed levels have been reached in some of these AI related names but in a vertical move as we regularly comment, the biggest move is often right before the end. Maybe we just had it! Much is made in markets of the need for analysis and intellectuality. Bears always sound clever (and generally remain bears). However, in a phase of the market as we find ourselves now, we draw attention to one characteristic that investment managers must have in abundance - GUMPTION. In order to hold through the types of moves we have seen one simply has to be very brave. This week we saw a sensational move in a name we have mentioned before, Marvell Technologies. After already more than 100% since March, it surged 30% on Tuesday and 50% this week (as of Thursday's close) as the man of the moment and Nvidia boss, Jensen Huang, mentioned in a public appearance with the Marvell CEO that it will be a trillion-dollar company. For a company which before that was trading on a market capitalisation of $180 billion, that is a looooong way to go. The good news is that thanks to Jensen it's a lot closer to the figure. This type of outcome is obviously symbolic of euphoric sentiment. Marvell, despite all its sexy narrative and legitimate transformative opportunity now trades on around 45 times earnings 12 months out. To the valuation crowd it is clearly on the high side. But why can't it go to 60? 100? The famous quote about the market being irrational longer than you can be solvent applies here. For us we always make sure we have an exit plan. The truth is that we really don't know what happens next. We just want to maximise our chance of running our winners while remembering that by this afternoon we could be out and in cash. And we really wouldn't give a damn either way.

The SpaceX hype is going to reach fever pitch next week as the IPO roadshow arrives. Apart from all the fuss around valuations and timing and market tops etc, we are about to enter into a watershed moment for the stock market. We are going to see SpaceX, Anthropic as well as OpenAI IPO. These are 3 defining companies of this era. Historic.

Also very worthy of mention this week is the once again pitiful performance of crypto. Bitcoin has collapsed anew and so has pretty much everything else. We have written extensively about our views on Michael Saylor and Microstrategy and it seems we are in the midst of what we are calling the Saylor Spiral. Microstrategy's first sale in many years has triggered a waterfall effect on Bitcoin given the entanglement between Microstrategy and Bitcoin (MSTR owns 3.5% or so of Bitcoin's supply). There is no real reason why Microstrategy needs to exist at all. And Bitmine Immersion and all their friends in the VC exit rat race. The endgame is nigh, and we are here for the fireworks. Ironically as all this unfolds there is continuous evidence that Bitcoin could actually end up being something really important. Once this Saylor fiasco is put to bed, there is reason to be optimistic given the continuous rollout of legislation and infrastructure around Bitcoin itself. But we are not there yet.

Meme of the week

Another indicator of where we are in the market is the performance of the MSCI Emerging Markets Index. Now we all know that EM is one big AI trade, right? Right? Well actually, it is. The biggest components of this anachronistic index are those very emerging countries of South Korea and Taiwan. It's been a joke for some time to be honest. But the reality is that TSMC and the Korean memory names, Samsung and SK Hynix are the biggest drivers of performance (and now 30% of the index). The real emerging markets like China... I'm kidding as we all know China is a superpower and most definitely not an emerging market anymore for a long time. The real emerging markets like Brazil, South Africa and Turkey have fallen 10-15% since recent highs. Indonesia, after 20 years of positive momentum and economic progress is having a nightmare. Its stock market is down nearly 40% in the past months. This is what happens in a real emerging market. Progress cannot be taken for granted, as one bad regime and it is all gone. DC

What we're reading.

When it comes to crypto, the key factor is the security of the cryptography itself. And up till now, because of the near infinite plethora of tokens around, finding exploitable gaps in cryptography was like finding a needle in multiple haystacks. Around comes our favourite AIs – in this case, using Anthropic’s Claude Opus 4.8, a Whitehat security researcher found a code exploit in Zcash, one of the major OG privacy coins. For those that aren’t familiar with this segment of the market, privacy coins were a segment of the crypto ecosystem that offered a solution for transactions to be provable but without exposing the parties and amounts involved, using what was known as a “zero-knowledge proof”. Unfortunately for them, this Whitehat operation located an exploit that allowed for unauthorised new token mints, present since May 2022. Yet because of the same privacy features that made it appealing, no one could cryptographically prove if that exploit had been used. Put differently, the privacy shield prevents anyone from proving if any counterfeit ZEC tokens had already gone into circulation, and if so, how many. For a token with a supposedly fixed supply, that doesn’t seem so fixed anymore. And thus, the joke starts going around Twitter: that there is zero knowledge nor any proof of exactly how many tokens are around. Kind of like someone adding extra chips to the casino but no one knowing for sure. Net result: -50% market cap in 2 days just because the crypto wasn’t cryptographically secure enough. Looks like crypto’s found its nemesis – and we haven’t even got around to quantum.

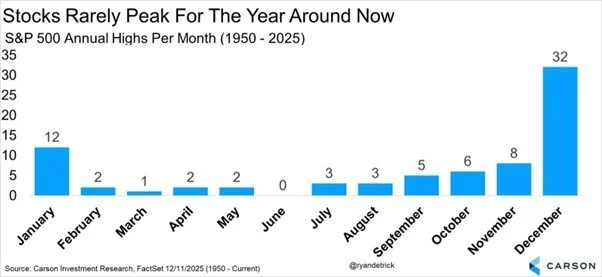

In other news, if statistics are to be believed, maybe we can all still enjoy these markets a bit more, because in the past 75 years (and of course, there’s always room for a first time), the market has supposedly never peaked in June. Yet. EL

What we're watching and listening to.

An excellent episode on the state of AI and the implications for the job market on the All in pod this week with David Sacks in particularly good form. He draws attention to the fact that job postings for software engineers are rising, something incongruent with the expectations of AI to lead to mass job losses. Could it be that the optimistic case is playing out? Way too early to know but it is lovely to see positive stuff in the sea of negativity.

Darius Dale on Forward Guidance this week is also worth a listen as he continues to lay out his bullishness on the US economy. This one gets into the nuts and bolts of US economic prospects more broadly and this guy is good.

And finally George Friedman with a very timely podcast on the fracturing of the US and Israeli relationship. He believes that despite the strong alliance between the two countries, objectives are diverging. Trump wants to bring the war with Iran to a close for his own reasons, but Israel cannot simply stop going after Hezbollah in Lebanon and leave its Northern population under attack and vulnerable to infiltration. Israel's necessity is to push Hezbollah far enough North so that they are not a threat, but Iran is insisting they will not end the war without a full cessation of hostilities in Lebanon. The focus this week was on a phone call between Trump and Bibi which went public, with an alleged shouting match between the two. It's difficult to see how this evolves. Good time to listen to the best man on the topic. DC