Life in passive? It’s reflexive.

Photo by Sean Bernstein on Unsplash

When we started Three Body Capital, we were conscious that the seeds had been sown for drastic changes in the way the world worked, not just in terms of the industry in which we operate, but also markets as a whole – and even society in general.

Almost three years on, it is clear that while we did foresee some of these changes, it remains a case of us finding even more profound (and subtle) forms of disruption the deeper we dig. Regardless of which rabbit hole you choose to take a peek into, whether into the world of crypto, NFTs, market structure in equities, derivatives – the gears are turning, taking the old ways out to the wash.

Yet if we have the wrong mental models, we will arguably never process the information we are given correctly.

There are many mental models that need updating, but when it comes to markets, we are arguably tipping over the threshold – in real time – from a mean-reverting world to a reflexive, passive-dominated regime. This passive dominance is what we’re revisiting this week.

Continuing down the current path means more of the dislocations that we see today: more passive, less active; more momentum, less fundamentals; more volatility and trend following; more of the tail wagging the dog.

Unfortunately, these changes aren’t transitory. More likely than not, they’ll snowball and accelerate over time.

The rise of passive money in the market, especially in US equities but equally true across the globe, is a phenomenon we’ve written about extensively but not for a while. The natural end point of that train of thought was always a line which would be entirely at home in films like the Matrix or Terminator: “What happens when the machines take over?”

No surprise then when we spotted these stats from GS earlier this month (thanks again to our friend Scott Rubner!). For the first time in history, US passive fund AUM has now fully exceeded active fund AUM, with USA Passive AUM at $4.636tn (52% of assets), and global passive AUM at US$7.565tn, breaking the $7bn mark for the first time. Passive inflows logged +US$606bn of inflows vs active funds +US$120bn YTD as of early this month.

The stats continue: Tech stocks saw 11 straight weeks of inflows, and in the context of passive funds’ “you give me money, I buy” vs “you ask me for money, I sell” mechanics, for the first 45 weeks of 2021 no one’s ask for any money, while giving passive funds a whopping US$951bn worth of dollars to buy.

With that as the backdrop, this tweet by Dan McMurtrie last week as the market seemed to be falling apart succinctly sums up the state of play in the investment management industry:

It has been our long-held view that the changes that are happening for investment managers are structural and probably irreversible. The landscape in which active managers operate is changing dramatically, resulting in many of the industry’s long-held beliefs and rules of thumb not really retaining their relevance.

Does this mean we chuck the old rules of risk management and sensible research out of the window and go full-blown YOLO? Of course not.

But they very much deserve a hard re-think.

The not-so-eternal tug-of-war

Historically, the search for balance in the market has been portrayed as a tug-of-war between participants that were largely in equilibrium. The balance would swing one way or the other but eventually, things return to the middle. Growth vs value, equities vs bonds, defensives vs cyclicals – to name a few.

The problem with active vs passive is that unlike the other tugs-of-war, the balance of active vs passive is reflexive.

Consider first the situation of, say, growth vs value: in this construct, typically existing under a framework of dominant active management (i.e. people looking at stocks and picking which ones to buy and sell), there comes a point at which the hunt for growth becomes so ridiculous that someone throws in the towel and sells. Many may remember the old “GARP” acronym: Growth at reasonable prices.

At that tipping point, the broad consensus becomes that growth is too expensive, and everyone else is crazy for paying up such multiples, and the shift towards value happens. This continues until enough people buy into “value” to make “value” no longer “cheap” (another output of people looking at stock screens and deciding some multiple is “cheap”), and the pendulum swings the other way.

The problem with active vs passive is that these are two diametrically opposed views of the world: “stock picking” vs “buying the index” are fundamentally incompatible with each other. They aren’t, unlike the other forms of equilibrium, “two sides of the same coin”.

Whether we adopt the argument of cost that passive is cheaper, or the self-fulfilling narrative that “traditional active management has on average underperformed the market” - despite the obvious statistical reality that in a distribution skewed to the downside, the mean is higher than the median – the generational shift of asset allocation from active to passive is unstoppable.

As a result, we don’t think this is a tug-of-war at all. It’s a one-way street, and as active managers ourselves, the route to outperformance is to recognise that the game has changed and play the hands we’re being dealt.

When in Rome, do as the Romans do

We do not for one moment profess the idea that we should behave like a passive algo. Rather, we need to be wary of being trapped by our tendency to work based on the “active algo”.

The “active algo”, you ask? Indeed, the algo that says that all stocks have an intrinsic value that can be determined through fundamental analysis and, most importantly, the party that gets to calculating that intrinsic value first enjoys the benefit of everyone else coming along to buy, netting a nice profit in the process. It may not be an algo that’s coded for computers and quant systems to run, but certainly over the years it has become etched in the mentality of investors and managers around the world.

Where the active “algo” perpetuated an equilibrium of mean reversion, passive perpetuates reflexivity – up means more up, and down means more down, and as we’ve written before, having only a tenuous relationship to the “fundamentals” that guided the processes of active managers.

As markets move from mean-reverting to reflexive, driven by dynamics that are absolutely non-human (or perhaps even “inhuman”), those of us who choose to remain in the space have to adapt at every level – or face extinction.

The mental models of reversion are pervasive in our thinking, and arguably it is this thinking that defines a lot of how we think about risk and performance.

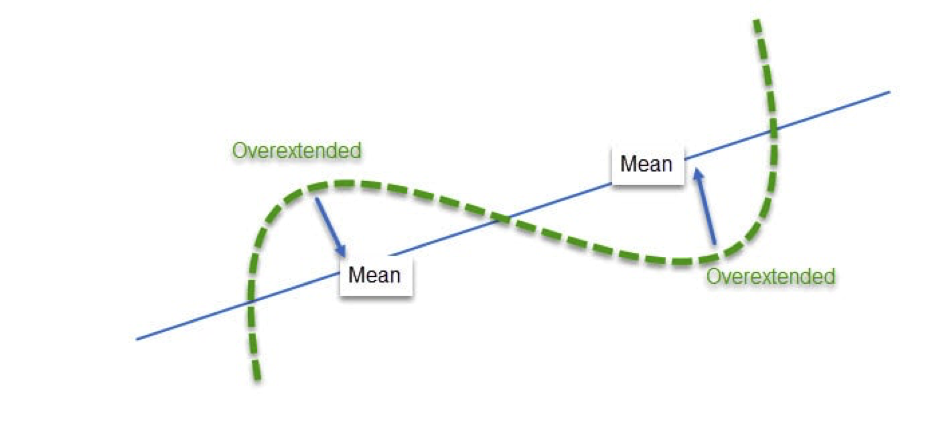

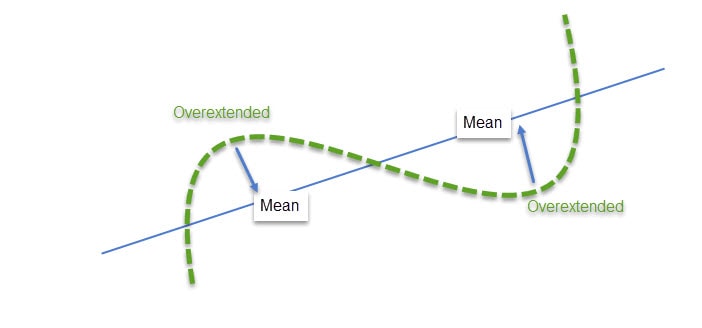

Traditional models of risk management, for example, use volatility as a proxy for risk, with the general rule that more volatility = more risk. The preference is for less volatility but with a “steady” upward trend, something that looks like this:

This would be true in a mean reverting world, but one look at the real world, at something like the S&P 500 ETF, would show clearly that such a strategy of expecting mean reversion can only end in tears. As is clear from the chart, finding (and timing) the dips in a passive-driven market is close to impossible. And “traditional” measures of what is overextended movement in either direction don’t apply either – certainly the 8% a year textbook expected return from equities doesn’t seem to apply here.

{kind=link}

At least this is true at the Index level. And investors have a very real choice to simply “just buy the ETF”, and they’re certainly not paying managers to buy ETFs for them.

The ongoing challenge for managers is how to continue to pick single stocks, which arguably have individual correlations to their own fundamentals in a much more defined way, while being compared to a benchmark that is inexorably liquidity driven and fully reflexive.

The end of human discretion?

Nonetheless, making the reverse argument – that the age of human discretion is over – also makes no sense. The top-down asset allocations that move money in and out of ETFs is ultimately a human decision. It is effectively the hunt for performance, albeit in a backward-looking but nonetheless self-reinforcing (and reflexive) manner, that is driving what we see today: seeking performance from lower costs (ETFs), while allocating to the best-performing assets on a historical basis (US equities) through a vehicle that perpetuates what is effectively a momentum strategy (market-cap weighted allocations).

These asset allocation decisions which exist at a higher level than index weightings may still fall into the realm of mean reversion – the tendency to look for “undervalued”, “emerging” themes to get exposure to will always exist. However, that they move back to previous favourites (for example, emerging market equities) is far from certainty. More likely than not, these same human tendencies lead to the search for new and shiny themes that make funds marketable to investors.

And let’s not forget the world of options, where there certainly exists room for human discretion. Whether in the land of retail equities, where (once more, credit to GS for the stats) options volume notional at the end of August was 120% of stock volume notional – read “tail wagging dog”; or in the land of institutions where the likes of Carl Icahn (selling S&P puts unhedged in the market) or JP Morgan’s gargantuan equities fund rolling over their hedges with massive collar strategies, these dynamics combined with the structural nature of passive inflows vs active outflows have a material impact on market behaviour.

We have known this was coming for a long time now, but the evidence is now clear: if we choose to remain in this space as managers, we cannot afford to be silo-ed into being a certain “type” of manager: a “fundamentals” manager, a “momentum” manager, a “thematic” manager etc.

To succeed, the bar is getting higher and we need to have eyes on EVERYTHING: from commodities to US rates, from FX to dealer gamma positioning, to the fundamentals of each instrument we hold in our book.

To that end, less is more when it comes to managing risk in a reflexive world: the age of the diversified portfolio of 60-100 instruments is gone. Not only is it physically impossible to properly go through results calls for 100 companies every quarter, the extensive correlation in the market that results from passive flows means the diversifying effects of having many instruments quickly wears off.

On the flipside, concentration means decoupling from the index in terms of near-term performance, with returns ultimately coming in spurts, with higher volatility along the way, rather than the textbook utopian dream of “just 1% a month”.

Once more, we run the risk of offending the investment management orthodoxy with such views. So be it, especially when the orthodoxy was from a prior age.

Past performance is no indication of future performance, as we all know.