Inflation: Numba still go up?

Photo by Mark König on Unsplash

It’s more or less official now: the narrative around inflation seems to have gone full circle, with markets moving to bet that the Fed needs to put in a rate hike sooner rather than later, or at least articulate some sort of plan for tapering of bond purchases.

“Wen taper? Wen rate hike?” ask the memes.

The credit market is reflecting this with little ambiguity. 10-year treasury rates, after taking a 2-month hiatus from their upward trajectory, seem to have caught their breath and look poised for more “numba go up”. Of course, the 10-year is just the easy benchmark: with the exception of super short term rates (e.g. 2-year maturity), ALL rates are exhibiting that same behaviour, looking poised to push higher.

Anecdotally, stories of Macdonald’s having to offer incentives to even get candidates to interview make the headlines, with similar stories being told by businesses all around - not just in the US, but also in most developed economies that see a glimmer of hope of reopening. The temporary measures put in place to protect incomes through the pandemic risk becoming a permanent feature, the covert introduction of a form of Universal Basic Income.

Added to growing commodity demand and the aforementioned movements in rates, the inflation narrative is going strong.

On the flipside, the Fed continues to push the narrative of “transitory” inflation, never failing to remind markets that the new rules of the game involve average inflation targeting. To that end, they are still justified by the macroeconomic data that is getting published: from PMIs to Non-farm payrolls to Initial jobless claims, numbers are looking better but to say that they are indicative of a healthy US economy would be inaccurate.

Where the Fed hopes that inflation is transient, on the other side of the world, Chinese policy has been unambiguously hawkish. From a slowing “credit impulse” to measures to contain commodity prices to outright warnings about “whimsical” stock market targets, amongst other constant reminders (for example, on the national Securities Times journal’s QQ account) that “numba go up” might have gone too far – albeit not in those exact words. 2021 is a particularly critical year for China, marking the 100th anniversary of the founding of the CCP. Stability is key – “numba go up” isn’t.

As we expected, 2021 isn’t anything like the one-way “up only” story of 2020. As always we look at the potential for things to pan out via multiple paths. So we’ll attempt to unpack some of those potential outcomes here and try to make sense of these moving parts.

Governor’s dilemma

To paraphrase the famous Prisoners’ dilemma in game theory, the choices the Fed faces in its game with markets are stark.

On one hand, it can choose to do nothing in the face of what the market (as well as ourselves) believes are unambiguous signs of inflation across all segments of the economy, on the premise that it has now changed its reaction function target to an average inflation rate as opposed to a “spot” rate. It is important to note that even the prior reaction function based on “spot” inflation as reported is already backward looking since data is reported to the Fed itself with a lag.

On the other, it can choose to be proactive – as it has attempted to do in the past, with slightly unpleasant consequences. Unfortunately, everything from the first mention of “tapering” and the subsequent “taper tantrums”, including attempts to slow asset purchases or simply allow assets to expire, have been met with an outcry from the market. No wonder then that the history of the Fed’s balance sheet looks like textbook “up only” too:

Source: https://fred.stlouisfed.org/series/WALCL

Critics of the Fed are quick to point the finger at populism, arguing that its independence has been compromised especially in the wake of the Trump administration’s prior focus on the performance of the stock markets as a barometer of the health of the underlying economy. While there is no doubt that such a correlation is spurious (ask those who lost their jobs in 2020), it is perhaps unfair to blame the Fed’s decision making as purely driven by a desire to keep the stock markets up.

What is often forgotten is that the debt that is being purchased by the Fed itself is the debt of the US government, the stock of which has also been, well… “up only”:

Source: https://fred.stlouisfed.org/series/GFDEBTN

In case this snapshot ends up showing up too small, the number at the end of that chart is US$28tn of total federal government debt outstanding.

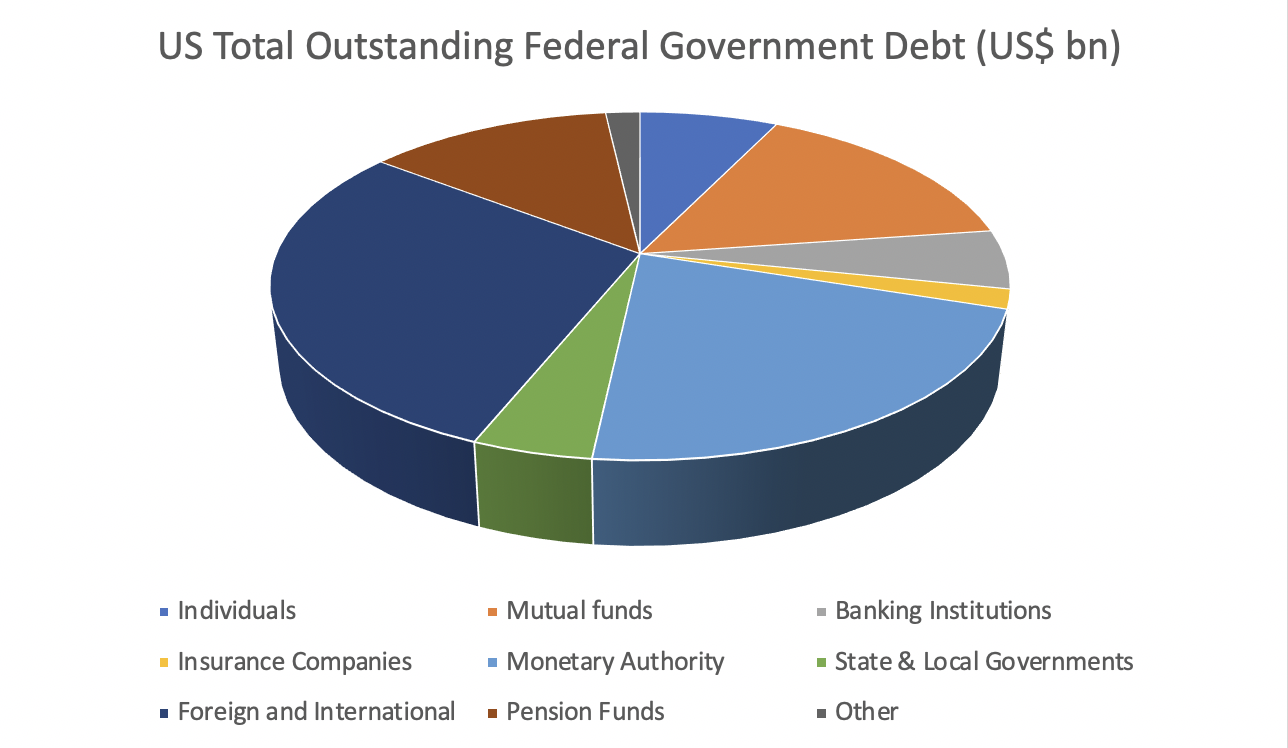

SIFMA data (up till 4Q20) allows us to break this down into individual holders of US outstanding government debt – while the numbers won’t add up to the real-time figures from the Fed, the holding pattern shouldn’t have changed much:

It suffices to say that given this distribution of holders of US debt, any moves on the part of the Fed to hike rates would lead to some very unhappy bondholders. The downside exists not just for the equity markets, but also in credit, including the layers of derivatives built on top of these markets.

The elephant in the room is the incremental cost of debt issuance, which has been put off to some extent as the now-famous “Treasury General Account” (TGA) has been drawn down in recent months to fund spending:

An observation on the side to be made here would also be that the recent escalation in the use of the Fed’s Reverse Repo facility to unprecedented extents could well be a function of a shortage of Treasuries available as collateral vs excess reserves coming out of the TGA. Some point to this to say that QE is reaching the limits of efficacy, with incremental QE taking too much collateral out of the market – that may be the case, although the flipside of that argument is that once the TGA balance is normalised, new debt will need to be issued again, creating the required supply of collateral.

Ultimately both threads of argument lead to the same end: debt needs to be issued one way or another and a higher rate benefits no one – not existing bondholders, not the Federal Government, not the banking system.

The Fed needs to hike, but hiking risks triggering the instability that the Fed is mandated to prevent.

“Money printer go brrr”

The mockery that the memes pour onto the Fed reflects the market’s growing belief that the Fed might be caught with its pants down again, just as it came to pass in 2007-2008. This time, the worry is that if the Fed doesn’t rein in inflation ahead of time and goes on with its plan of average inflation targeting, it will be too little, too late by the time the tightening comes. And the money printer actually gets out of control.

One way this entire situation plays out is that the Fed suddenly does a backtrack on its “no hike” stance, starts turning hawkish and succeeds in putting the inflation genie back in the bottle – at least temporarily. A transient containment, insofar as their commentary continues to carry weight and their credibility remains intact. The US Dollar stays strong, although it’d be bad news for almost everyone else.

For the believer in central bank independence, that’s the ideal scenario.

The other side of the coin is that the Fed sticks to “no hike”, based on its data-driven approach. It wouldn’t stop the market from pushing yields up, but such a decision would likely bring on pretty adverse outcomes for the US Dollar itself, which does change the dynamic for everything outside the US.

The biggest winners here would be commodities and emerging market cyclicals – there is nothing better than a weak USD for all of them, and as long as the underlying trajectory of commodity consumption continues in a world that is reopening and enjoying low base effects from last year, there could be light at the end of the tunnel, especially for the likes of India and Brazil, which have been ravaged by COVID over the past year and are now starting to see a glimmer of hope.

Tech on the other hand, especially unprofitable operators, may find themselves somewhat out of fashion as the rising rate dynamic comes back into play one way or another.

And what of China’s negative credit impulses and their countercyclical dampening efforts?

One could argue that such policies are exactly what a central bank should be doing: keeping animal spirits in check, especially on an important year like 2021 when the CCP’s track record of delivering stability and prosperity for all is on display. Furthermore, while still a large consumer of global commodities, to expect the same trade now as when the “commodity supercycle” came to an end with China’s re-orientation towards services from manufacturing would be a bit of a fallacy.

Sometimes we can do the same trade twice – this is likely not one of those times.

Finally, what about crypto, one may ask?

Incidentally, as recent moves have demonstrated, crypto largely dances to its own tune. One could argue that a weaker USD does help, although for many projects the underlying growth trajectory far outweighs the implications from global macro. Bucketing them under “unprofitable tech” is also a fallacy – as we’ve highlighted before, there are some highly profitable protocols in the space. The past few weeks have seen large amounts of risk flushed out from the system, giving crypto a much cleaner slate to work from than most other markets.

With this many moving parts and potential outcomes, we fall back on process to guide our decisions: price action remains our guide, and conscious that the road ahead is long and winding, with a few sharp corners along the way, we tread lightly and carefully, always open to the possibility that things may change at quite literally the blink of an eye.