Weekend Reading #195

Photo by Priscilla Du Preez on Unsplash

This is the hundred-and-ninety-fifth weekly edition of our newsletter, Weekend Reading, sent out on Saturday 19th November 2022.

To receive a copy each week directly into your inbox, sign up here.

*****

What we’re thinking

You’ve probably been reading about it everywhere but we cannot help but write a lot about SBF/FTX again this week. What a mess.

The world of crypto is working hard to rebuild from the fallout but the reality is trust lost is hard to regain, and while the logic of DeFi having been corrupted by centralisation (e.g. with FTX) is well understood within the crypto community, the sad truth is for everyone outside, this is a case of “crypto collapse = crypto is a scam”, and the risk aversion that comes from this is likely to weigh on the prospects for new inflows for some time. The market is going to take time to work out what the correct solution is from here, but we’re sure it will get there. Eventually.

Silver lining? Lower prices. For now, the dominoes continue to fall: most recently in the firing line was DCG, particularly its subsidiary, crypto trading firm and market maker Genesis, reportedly now in the process of trying to secure a US$1bn funding line to bridge a withdrawal gap. The immediate impact: Genesis was the source of the “yield” being offered on Gemini’s Earn platform, which has now suspended withdrawals. But the bigger problem is this: Genesis was also one of the biggest authorised participants in DCG’s other products, better known as the Greyscale trusts, particularly GBTC and ETHE which themselves own c. $13.3bn and c. $3.7bn of BTC and ETH respectively in the trust. These already trade at significant discounts to NAV c. 40%, and selling pressure from a Genesis trading book unwind is unlikely to do that discount any favours. Unfortunately, though, GBTC was one of the few instruments that were permitted as BTC exposure in the average 401k account. We’ll find out how this pans out in the days to come.

But perhaps the most fascinating bit of the FTX story so far is that SBF remains free to do as he pleases in the Bahamas, including being allowed to tweet freely on his account while reportedly sometimes showing up for a game of League of Legends. Furthermore, it turns out that SBF wasn’t even that good at League, with Congresswoman AOC ranking higher than him.

Levity aside, one can only be left to wonder why enforcement action has been so timid. Perhaps even more puzzling is how the mainstream media has been so gentle with SBF: this piece in the New York times came off as almost being an SBF apologist piece, while Reuters actually printed an opinion piece titled “Sam Bankman-Fried did financial system a favour”. Conspicuous in its absence: the use of the words “fraud”, “theft”, “embezzlement” or in fact anything with a negative connotation. Likewise, nothing from the regulators: the CFTC chairman Rostin Behnam was given a platform on CNBC and all he had was minutes of equivocation, fuelling speculation that SBF’s political donations and connections are very much in play here.

There’s one exception: Bloomberg’s Matt Levine on the Odd Lots podcast was probably the only straight-shooting character to talk about this in the context of fraud, ponzis and criminal prosecution, so kudos to that.

Already, the cries of inconsistency and allegations of regulatory capture are mounting, as pointed out by David Marcus, formerly of the payments/crypto team at Facebook (at the time) and on the Libra team (remember Facebook wanted to launch a stablecoin?), who recalls being summoned within 24h of dropping the Libra whitepaper to testify in front of the Senate and the House, and compares that to the lack of enforcement action being seen now.

Most succinctly, this tweet sums up how the regulatory enforcement regime is being perceived at the moment:

But the biggest surprise came when we saw Kyle Davies of Three Arrows Capital infamy appearing on CNBC too, emerging from the shadows to lay blame for 3AC’s collapse on FTX, accusing Alameda Research of hunting their stops, causing them to lose money, and publicly calling for truth and justice. CNBC’s Becky Quick, perhaps true to her last name, took no prisoners with this question: “Are you located in Bali because Indonesia is one of the seven countries that won’t extradite you to the United States?”.

What a winner. What a joke. What a disaster.

Crypto aside, volatility in the equity markets continues to become the norm. And while it is understandable that exchanges want to offer customers more products to make more money (in the name of “democratising access to markets”), one has to consider what the equivalent of increasing widespread distribution of firearms does to an already-tense society in the name of providing a “level playing field”.

We’ve written about how the dramatic moves in Gamestop were driven by the options market, and in recent weeks pointed to how options activity is suggesting that the use of 0 days to expiry (aka 0DTE) options is now spreading to the index level, with the associated hedging flows driving much greater index-level volatility. Well, where the term “0DTE” didn’t use to be specifically mean “zero days”, but rather close to zero i.e. “very soon”, the CBOE has now decided to make that definition perfectly accurate, with Tuesday and Thursday weekly SPY and QQQ options starting to trade this week. Changes like these to market microstructure are profound because they permanently impact how participants behave.

Of course, this was part of the plan, as CBOE mentioned in their Q3 results:

What’s the risk of it all? This short video by SpotGamma explains it pretty well, with a longer Q&A for those who are keen to spend a bit more time on it here that was very helpful.

What we are reading.

A while back, I shared a podcast with a chap named Antonio Garcia Martinez, who had one helluva story (He was the Apple employee who got chucked out for writing a book which contained what was considered to be “anti-woke”). He originally piqued my interest due to his decision to pack up and head off to Ukraine early in the war to see for himself what was going on. I mean, who does that? His comment early Friday on Twitter about Elon Musk shaking things up is absolutely spot on. If Elon succeeds here, there is precedent for almost every company in Silicon Valley to weed out thousands of employees who are quite simply not only not pulling their weight but adding substantial baggage to the workweek. I continue to hope Elon succeeds here regardless of all his other stuff. DC

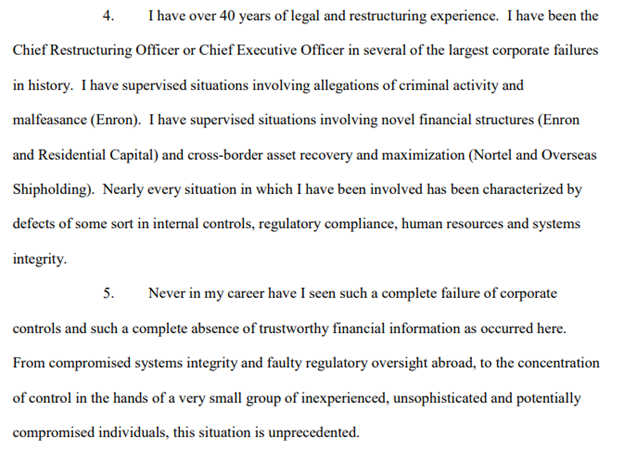

How do you know when something bad is REALLY bad? Perhaps when the person that dealt with the last worst thing says so. As it stands, the initial Chapter 11 filing from FTX’s new CEO, John J Ray III, has just landed, filed on the 17th of Nov, just about a week after taking over as CEO. The stunning details start from statement 50 on page 18 onwards, but suffice to say that without going that far, just on page 2, we find his indictment of SBF and FTX management in as plain English as it gets, in the superlative. It took them a week to work these things out, or rather to work out that controls and systems for an organisation of this scale simply didn’t exist. Sure, in a bankruptcy procedure, the books are wide open, but shouldn’t they be so as well during VC due diligence under an NDA? All this then leads to the question of how the great investors like Sequoia and Temasek, having had months to do due diligence on FTX, didn’t manage to work these shortcomings out. This anecdote from Chamath on the all-in podcast, keeping in mind that Chamath is as high-profile as it gets, leaves one wondering if the questions he asked were even posed to FTX by everyone else, or whether they were so enamoured by the appeal that they, too, were guilty of a poorly thought out YOLO decision.

As far as comeuppances go, remember this photo that was going around the past few years?

From FTX’s early days, this photo itself became a meme, which until recently used to represent the David vs. Goliath situation that panned out in the land of crypto exchanges: Sam Bankman-Fried in his younger days facing off against Arthur Hayes of BitMEX fame, the “new blood” staring down the “old blood” and seemingly, for a time, winning.

Well, not anymore. Arthur Hayes’ writings are some of the most enjoyable (if not some of the most pointed, sharp and acerbic) writing in the space. And this week, he is having a field day, publishing part 1 of what he promises to be a 2-part essay on how the persona of SBF came to be, and how SBF and FTX managed to become the giant that it was, before crumbling to bits. So far, in true Arthur Hayes style, Part 1 does not disappoint – no spoilers here, it is best enjoyed without too much introduction, especially because he pulls no punches. EL

What we’re listening to.

Mike Green has been a source of great instruction when it comes to our understanding of market structure, especially given his prior work on passive flows and options-driven market behaviour. This podcast on Macro Voices, however, features Mike Green in a slightly different element, looking at geopolitics and the ongoing (and growing) conflict of ideologies and societies, mainly between the US, China and Russia, but really in the grand scheme of things also with a myriad of other countries jostling for places in a rapidly evolving world order. Pax Americana, to which Arthur Hayes refers to in his SBF essay, is not the way it used to be, and the implications on capital flows, market structure and all aspects of life (for we cannot be fully detached from the economy, can we?) are profound and long-lasting. This may not (for the moment) entail a full-blown nuclear Armageddon, but this conflict isn’t “cold” either – flashes of “hot” conflict look to become more, not less, frequent, and that all just means more volatility in outcomes and in markets. Very much worth a listen. EL

What we’re watching.

One of the best shows on TV is undoubtedly Peaky Blinders. It’s one of the few that I missed originally and have actually kept going with to catch up. I’m on season 4 now and it's just brilliant. Cillian Murphy who plays Tommy Shelby, the main character, is superb. As many may know he is more than just a bit odd. He is privacy obsessed and does not give interviews. His intensity is just insane. The intrigue, the intricate plot, the music and the characters are just brilliant. And as season 4 got going, Adrian Brody popped up to play one of the Italian mafia characters, Luca Changretta. What a show. DC